Car modifications are often seen as an expression of individuality and performance enhancement. However, when it comes to insurance, the implications of these modifications can be significant. From performance tweaks that transform your vehicle’s capabilities to cosmetic upgrades that enhance its appearance, every modification has a potential impact on your insurance premiums and coverage. We’ll explore how different types of modifications affect your insurance, clarify the importance of legal compliance, and highlight the necessity of full disclosure with your insurance provider. This comprehensive guide aims to empower hobbyist car modifiers, professional tuners, and enthusiasts alike to navigate the intricate relationship between car modifications and insurance.

How Performance Mods Change Your Insurance Profile: Risk, Disclosure, and Cost

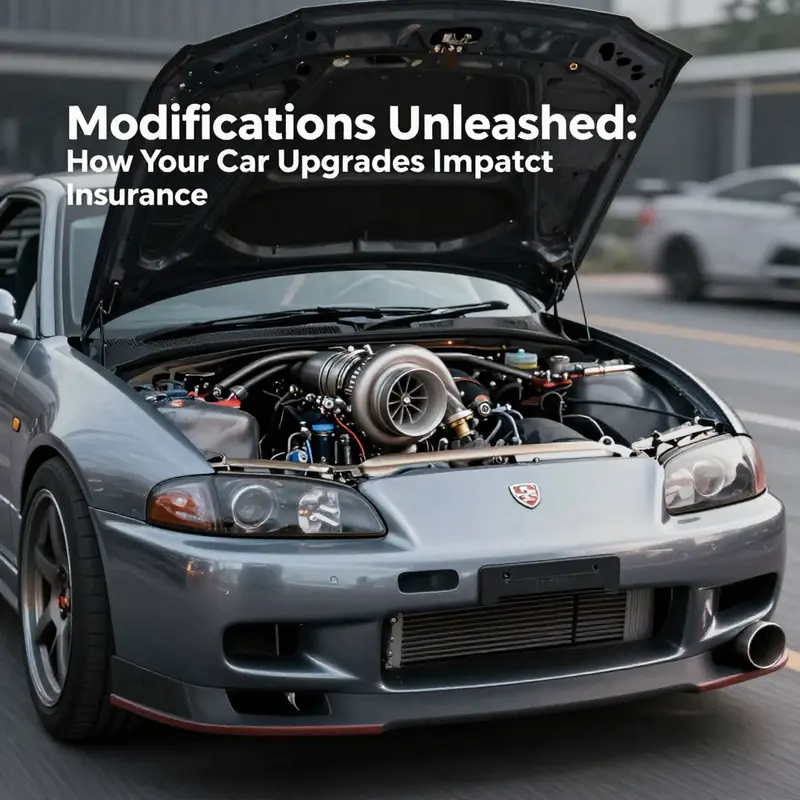

Performance modifications transform a car’s character, and they transform how insurers see it. Upgrading an engine, bolting on a turbo, changing the suspension geometry, or fitting a freer-flowing exhaust does more than boost lap times. It alters the vehicle’s safety envelope, failure modes, and the likelihood of collision. That shift in risk profile drives the insurance industry’s response: higher premiums, special endorsements, or outright refusal. Understanding that response helps you plan upgrades, avoid costly surprises, and maintain coverage when you want it.

When insurers assess a modified car they ask a simple question: does this change increase the probability or cost of a claim? The answer depends on three factors: the nature of the modification, how it affects safe operation and reliability, and whether the change is declared. Minor bolt-ons like a cold air intake or a cosmetic exhaust may barely move the needle. Major interventions—turbochargers, engine swaps, roll cages that alter structure, or lowered suspension that damages handling—do. Those larger changes increase potential repair costs and raise the chance of a severe accident, which insurers price into the policy.

Risk is not binary. Many performance upgrades sit on a spectrum where context matters. A modest ECU remap tuned for reliability can be very different from an aggressive tune that raises boost pressure to the limit. A professionally installed suspension upgrade with documented geometry settings and upgraded brakes can be less risky than a DIY lowering job that scrapes on speed bumps. Insurers examine the details: documented parts, professional installation, whether safety systems remain intact, and whether the modification is legal. These granular facts can determine whether your policy only costs more or becomes void.

Disclosure is the single most important behavior for anyone modifying a vehicle. Insurance contracts typically require you to inform the company of material changes to the vehicle. Failing to declare a performance upgrade can lead to claim denial even when the modification didn’t cause the accident. In many jurisdictions insurers expect written notification within a specified window after the change. Missing that window removes your ability to claim for losses tied to modified parts, and in extreme cases can lead to cancellation for misrepresentation. The simplest way to protect yourself is transparent communication: notify the insurer before or immediately after the work, provide receipts and installation details, and be honest about the intended use of the vehicle.

Premium adjustments reflect both probability and severity. For common performance changes, insurers will consider how likely the upgrade is to cause a loss, and how expensive repairs or replacement will be. Engine upgrades and forced induction increase top speed and acceleration, which historically correlate with higher accident frequency and severity. That leads to larger increases in premiums. Suspension changes, if they degrade ride height or stability, raise concerns about braking and control and therefore receive scrutiny. Conversely, some upgrades can reduce perceived risk. Fitting a reliable tracking device, after-market anti-theft measures, or advanced driver assistance systems may mitigate insurer concerns and slightly offset the cost of other mods.

Not all companies respond the same way. Underwriting guidelines vary between insurers. Some will offer specific modified vehicle coverage or an endorsement that explicitly covers performance parts. Others may refuse any policy on heavily modified cars, or exclude modified components from cover. Shopping around is critical. An insurer that specializes in performance or classic cars will have experience assessing aftermarket work and may offer competitive terms. When comparing offers, get the insurer’s position in writing, and clarify whether the cover applies only to parts, or to the whole vehicle and third-party liability too.

Beyond premiums, performance modifications can affect other financial protections. Manufacturer warranties are often voided by major engine work or electronic remaps. That increases the owner’s exposure to repair costs that would otherwise be covered. Resale value also shifts unpredictably: a tasteful, well-documented upgrade may attract buyers and command a premium, but extreme or amateur modifications often shrink the pool of purchasers and depress value. That lower resale value can indirectly influence insurers’ assessments, since the market value of the vehicle is part of the claims calculus.

There are legal and compliance dimensions too. Modifications that contravene local vehicle standards—such as tampering with emissions controls, removing critical safety structures, or installing lighting that violates regulations—can void coverage. Insurers will not pay for losses arising from illegal modifications, and in some cases may refuse liability cover if the alteration contributed to an accident. Before committing to any significant performance work, check regulatory rules and ensure the parts and installation meet law and safety standards.

Practical steps reduce surprises and protect coverage. First, document everything: receipts for parts, invoices for professional installation, detailed descriptions of software remaps, and before-and-after vehicle condition photos. Second, inform your insurer in writing and request confirmation of how the change affects your policy. Third, ask whether an endorsement or additional equipment policy is necessary to cover the upgrade’s replacement cost. For expensive engine work or custom fabrication, this additional policy often makes financial sense. Fourth, consider safety-led upgrades such as improved brakes, upgraded tires rated for the extra power, and functional roll protection that is professionally installed; these can be persuasive to underwriters.

DIY modifications raise special issues. Amateur wiring is a common source of electrical fires; improperly fitted turbo plumbing can fail catastrophically; and suspension adjustments without proper alignment produce unpredictable handling. If you install parts yourself, retain evidence of your competence: workshop manuals followed, torque settings observed, and photographs of the work. Insurers care about the cause of a failure. A well-documented DIY job performed to industry standards will be treated differently from a sloppy or undocumented effort.

If your insurer refuses coverage for heavily modified vehicles, there are alternatives. Some specialty insurers underwrite modified and performance cars. These policies often include agreed value coverage and endorsements for aftermarket parts. Another option is a trade-off approach: keep primary liability coverage while purchasing separate, limited coverage for modifications. Regardless of route, ensure clarity about how the policy treats performance upgrades, collision claims, and theft or fire involving aftermarket components.

Finally, think beyond the immediate. Performance modifications are often cumulative. Multiple small upgrades can collectively change how the vehicle behaves. Disclose changes as they occur so underwriting reflects the vehicle’s true state. If you plan future upgrades, discuss them with the insurer up front. Some providers will offer a path to keep coverage as you gradually modify the car, provided you maintain documentation and abide by safety and legal standards.

For additional authoritative guidance on regulation and insurance implications of vehicle modifications, consult the national safety agency’s resource on vehicle modifications and insurance implications: https://www.nhtsa.gov/vehicle-modifications-and-insurance-implications.

For practical information on finding coverage tailored to modified vehicles, see this guide to insurance for modified cars, which explains common insurer positions and endorsements: https://modifiyeliarabalar.net/blog/insurance-for-modified-cars/

When Looks Matter: How Cosmetic Car Modifications Change Your Insurance Risk

Cosmetic modifications are often the first changes owners make to personalize a car. New wheels, a striking paint job, body kits, or an upgraded audio system can completely change a vehicle’s character. Insurers know this. They also know that while many cosmetic changes do not alter a car’s core mechanical safety, they still influence risk, valuation, and claims outcomes in meaningful ways. Understanding how and why insurers react to cosmetic work helps you avoid surprises, keep your cover valid, and protect the investment you’ve made in both the car and the modifications.

Cosmetic changes are a broad category. They range from purely visual tweaks—paint, wraps, decals—to additions that affect the vehicle’s external profile, like spoilers, widebody kits, and aftermarket bumpers. Interior enhancements such as custom seats, re-trimmed panels, custom dash work, or high-end audio systems also fall under the same umbrella. Even obvious aesthetic choices like tinted windows or aftermarket lights can create a different underwriting response depending on local regulations. The first thing to remember is that insurers assess cosmetic modifications not only for direct safety impacts but also for secondary effects: increased theft risk, higher repair costs, and the chance that a modification conceals or masks other, more significant changes.

Repair cost and parts availability are two of the clearest reasons cosmetic mods increase insurance exposure. Standard parts are mass-produced and easy to source. Custom paint, wrapped panels, or bespoke body kits often require specialist repair shops, custom paint matching, or even replacement of entire panels. Insurers price policies partly on the expected cost to return a vehicle to its pre-loss condition. When a simple fender bender becomes a custom-paint job with color-matching and labor from a specialist, the insurer’s expected payout rises. That expectation commonly translates into higher premiums or the need for additional endorsements that explicitly cover the value of the modified parts.

Another factor is how visible modifications change the car’s attractiveness to thieves and vandals. High-end audio systems, custom wheels, and flashy paint schemes can make a vehicle a target. Insurers will often treat such vehicles as higher theft risk, especially if the modifications are easily removable or if the car’s security features were not upgraded to match. This is why insurers ask detailed questions about stereo systems, wheels, and security upgrades when a policy is written or when modifications are added.

Not all cosmetic changes are equal in the eyes of an underwriter. Wheels and tires are a good example. Fitting larger-than-standard wheels or switching to a low-profile setup can change braking performance and steering response. These alterations may increase the likelihood of loss or lead to higher repair bills if a collision damages expensive rims or specialized tires. Insurers want to know about such changes so they can determine whether to adjust the premium and whether any exclusions apply. Similarly, body kits or spoilers that require cutting or altering OEM mounting points move beyond cosmetic into structural change. Anything that affects crash behavior, airflow, or airflow-induced stability triggers a more rigorous assessment.

Interior modifications have a mixed effect. Replacing factory seats with racing seats might seem purely cosmetic, but if they remove or disable airbags or alter the proper operation of seat belts, they can increase injury risk. Insurers may decline liability for certain injury-related claims where safety equipment has been compromised. Likewise, bespoke electrical installations for sound systems or lighting must be done correctly. Improper wiring can cause short circuits and fires. If a fire is traced to amateur or non-compliant wiring, the insurer may deny the claim on grounds of negligence or because the modification violated policy terms.

Legality is a cross-cutting concern that affects cosmetic mods as much as mechanical ones. Local laws govern permitted window tint levels, the color and intensity of lights, bumper height, and more. A cosmetic modification that breaks the law places you outside the terms of most policies. That can lead to claim denial or even policy cancellation. This legal dimension also ties to resale value. An obviously illegal or very niche cosmetic package may narrow your market and lower the car’s insured value over time. Insurers consider the likely value at settlement, which is influenced by how desirable and how standard the modified components will be in the wider market.

Transparency is the single best control you have. Most insurers require written notification of any modification within a set window—often ten days. Failure to notify can create grounds for excluding coverage for modified parts or for voiding a claim outright, even when the incident had nothing to do with the modification. When you inform your provider, expect questions: What exactly was changed? Who did the work? Were original parts kept? Are the modifications permanent or easily removable? Be ready to provide receipts, photos, and installer details. For high-value visual upgrades, insurers may ask for an additional equipment endorsement or a standalone rider that covers the added value of customized parts.

A practical approach to managing insurance exposure from cosmetic mods combines documentation, compliance, and selective coverage. Keep thorough records of every modification: invoices, materials lists, and installer certifications. Use reputable shops that provide written warranties and comply with electrical and safety standards. If a modification affects a regulated item—like lighting or window tint—verify local laws first and ensure compliance. Consider fitting anti-theft devices or CCTV if the modification raises theft risk. When discussing cover with your insurer, ask specifically whether the policy will cover replacement at market value, new-for-old, or only the factory specification. For expensive cosmetic investments, ask about an “additional equipment” endorsement to protect the actual cost of replacing custom parts.

There are also strategic decisions to make about which modifications to disclose. While honesty is crucial, not every minor aesthetic tweak will change your premium. Small cosmetic items that do not increase replacement cost or risk may not need formal declaration. Still, a sound rule of thumb is to declare anything that adds significant value or modifies repair complexity. If in doubt, disclose. Put it in writing and retain a copy of the communication.

Finally, keep in mind the interaction between cosmetic modifications and other constraints, such as finance and lease agreements. If your car is financed or leased, the lender or lessor may have rules about permitted modifications. Unauthorized changes could breach those agreements and create additional liabilities beyond insurance implications. For guidance on how declarations and lender rules interact, review resources on declaring modifications to your insurer to make sure you follow the correct process and protect both your coverage and your contractual obligations: declare modifications to your insurer.

An insurer’s view of cosmetic modifications balances three things: the expected cost of repair, the impact on safety and theft risk, and legal compliance. Cosmetic upgrades that increase repair complexity, make a vehicle more attractive to thieves, or breach safety or local regulations will likely raise premiums or require special endorsements. Conversely, tasteful, compliant, well-documented work performed by reputable professionals can be insured with minimal friction, provided you communicate clearly and secure appropriate cover for the added value and risk.

For a concise overview from an industry perspective on how cosmetic procedures and similar modifications can affect insurance underwriting and claims handling, see the Insurance Information Institute article referenced below.

External reference: https://www.iii.org/article/cosmetic-procedures-and-insurance

Inside the Car, Inside the Policy: How Interior Upgrades Shape Insurance Choices

Inside the car, the small details of an interior modification can ripple outward in surprising ways, shaping not only the way you enjoy your ride but also the terms of your coverage when trouble comes. Insurance is, at its core, a risk assessment. It weighs not just how a car behaves on the road, but how its value, repair costs, theft appeal, and even its safety dynamics shift with every added feature. When the aftermarket and the factory meet inside the cabin, the result is a recalibrated risk profile that can push premiums higher, alter claim eligibility, or, in rare cases, prompt policy adjustments. For many drivers, interior upgrades feel like personal expression or improved practicality, yet insurers consider these changes through a lens focused on probability and consequence. The key is to understand the relationship between value and risk, and to communicate clearly with the insurer about the scope and intent of every modification.

The most apparent effect of interior modifications is often the change in the vehicle’s perceived value. A cabin finished with premium materials, custom upholstery, or bespoke storage solutions elevates the car’s replacement cost. While higher appreciated value can be a source of pride, it also raises the potential loss in a total loss scenario. Insurance generally aims to restore the insured to a similar position as before the incident, which means the cost of replacing customized elements now factors into the policy. This consideration goes beyond simple replacement; it shapes how comprehensive and collision coverages are priced and how deductibles interact with the overall settlement. If the interior upgrade is extensive enough, the insurer may require value verification, receipts, or even a professional appraisal to quantify the added cost. In turn, the premium may reflect not only the base vehicle’s value but the upgraded interior as well, especially if the upgrade changes the car’s categorization in the insurer’s risk pool.

Yet value is not the only axis along which interior modifications influence insurance. The more critical concerns relate to safety, security, and repair practicality. An interior that’s tailored with high-end audio or luxury fittings can attract thieves, increasing theft risk and potentially the likelihood of a comprehensive claim. The appeal of visible luxury inside the cabin translates into a higher probability that a vehicle becomes a target for break-ins or theft of components. In response, insurers may adjust coverage terms, require anti-theft devices, or propose different deductibles. The impact varies by jurisdiction and policy, but the underlying logic is consistent: theft risk rises with interior value, and that shift is reflected in pricing or policy terms.

Distractions and driver safety are another important thread. Interior modifications can inadvertently affect visibility, focus, or even the driver’s physical interaction with the vehicle’s controls. For instance, dashboards modified to accommodate larger displays or specialized lighting can create glare, obstruct important gauges, or divert attention from the road. Complex wiring for entertainment or ambient lighting installations introduces a potential fire risk if wiring is not executed to code. Insurers scrutinize how these changes might influence accident risk. If an alteration compromises airbag deployment, obstructs safety systems, or introduces a distraction that increases the likelihood of a collision, it becomes a safety concern that can raise premiums or, in rare cases, challenge coverage while the risk is reassessed.

The legality and quality of installation also matter greatly. A modification that complies with national regulations and industry best practices is far more likely to be treated as a standard risk adjustment than one that lacks proper certification or is DIY-stitched without expertise. When interior projects are not installed to recognized standards, repair and replacement costs may rise after a claim, and the insurer may view the modification as a complicating factor in determining fault and liability. The financial consequences of poor workmanship can extend beyond the immediate claim to ongoing premium calculations, as the long-term reliability of the vehicle becomes part of the risk equation.

From a policy perspective, disclosure is the hinge that keeps coverage intact. The principle is simple but critical: tell the insurer about each modification in writing, with as much detail as possible, within a reasonable timeframe. The absence of disclosure can transform a minor alteration into a breach of policy terms, potentially voiding coverage for damages to the modified parts or, in some cases, invalidating the entire policy after a loss. This is not merely a procedural formality; it’s a fundamental risk-management step that protects both sides. When details are omitted, the insurer may assume greater uncertainty about the vehicle’s risk profile, which can translate into denial of a claim or aggressive settlement terms that don’t fully reflect the consumer’s understanding of the modifications.

To navigate these complexities, many drivers consider seeking an endorsement that explicitly covers interior modifications. An interior modification endorsement acknowledges the added value of customized features and aligns coverage with the actual risk profile of the vehicle. It helps ensure that in the event of total loss or damage, the insured receives appropriate compensation for both the base vehicle and the modified interior. This approach reinforces the idea that transparency is not merely about avoiding trouble at the point of claim but about obtaining fair, accurate, and timely settlement when it matters most. It also encourages ongoing communication with the insurer as modifications evolve, ensuring that coverage tracks the vehicle’s use and value over time. The endorsement acts as a safety valve, preventing disputes that could otherwise emerge if a modification’s impact on value or safety were assessed only after a loss.

Relating these considerations to everyday ownership, the practical steps begin long before a shipment of receipts arrives in a file. Owners should maintain thorough documentation: detailed descriptions of each interior upgrade, dates of installation, installer credentials, and all related invoices. Photographs that document the condition of the interior both before and after modifications can be invaluable in the event of a claim. If you’ve added components that affect seating, restraint systems, or dashboard configuration, preserving documentation about how the installation aligns with safety standards is especially important. Warranties on aftermarket components can also influence how a claim is processed. Some components may be eligible for replacement through the same vendor network that supplied the upgrade, while others may require independent repair shops with specialized facilities. In any case, having a clear paper trail reduces ambiguity and speeds up the claim process, helping both insurer and insured reach a fair outcome.

Amid all these considerations, open dialogue with the insurer remains the cornerstone of responsible ownership. The moment you anticipate or execute an interior modification, initiate an honest conversation with your agent or underwriter. Explain the purpose of the change, the scale of the upgrade, and your plans for maintenance and upkeep. If the modification creates new storage or organization functionalities, emphasize how these changes affect daily use and crash dynamics. If the vehicle now incorporates high-value materials or devices, discuss theft-prevention measures and audit the security implications with the insurer. This proactive communication can pave the way for a more accurate premium that reflects reality rather than a best-guess assessment based on the unmodified vehicle. It also helps ensure that you understand any conditions tied to the coverage, such as requirements for professional installation, periodic inspections, or limits on certain types of components.

The idea of an internal modification endorsement is particularly compelling when interior upgrades are substantial. It acknowledges the dual reality of modern cars: the cabin is not just a space for comfort; it is a critical component of the car’s value, safety, and risk profile. A formal endorsement provides clarity for both sides and reduces the likelihood of friction if a claim must be filed. For many policyholders, this translates into confidence—knowing that the story of their car’s interior has a documented, agreed-upon place within the contract. It is a practical way to ensure that the new features, which often represent a significant personal and financial investment, are protected by insurance in a straightforward and predictable manner.

For readers seeking concrete guidance, a useful starting point is to examine resources that address how interior upgrades influence coverage. One practical step is to consult resources specifically focused on understanding modifcations and insurance, such as articles that walk through the nuanced ways insurers treat enhanced interiors, from theft risk to repair cost implications. This can help you frame your conversations with your insurer, prepare the necessary documentation, and determine whether an endorsement is appropriate for your situation. Insurance for Modified Cars provides a foundation for understanding these dynamics within a broader discussion of vehicle customization and risk management.

Ultimately, interior modifications sit at the intersection of personal expression, practical utility, and financial prudence. They offer genuine benefits—improved comfort, enhanced practicality, and a more personalized driving experience—while introducing new variables into the insurance equation. The responsible path treats these changes as part of a living risk profile: disclosed, documented, and aligned with a policy designed to reflect value, safety, and actual exposure. When done with foresight, these upgrades can coexist with solid insurance protections, ensuring that your prized cabin remains both a source of satisfaction and a sound financial position should the road throw a curveball.

External resources for a broader perspective on modifications and coverage can deepen understanding and support informed decisions. For a comprehensive overview of the landscape around vehicle modifications and insurance, the Insurance Information Institute offers detailed research and guidance that illuminate how insurers view these changes in practice. Their analysis helps bridge the gap between personal expectations and industry standards, aiding policyholders in navigating the delicate balance between customization and protection.

External resource: https://www.iii.org/article/vehicle-modifications-and-insurance

The Fine Line: How Legal and Illegal Car Modifications Redefine Insurance Outcomes

Modifications to a car are rarely just about speed, style, or convenience. They rewrite a vehicle’s risk profile in the eyes of an insurance underwriter, and they can tilt the balance between affordable coverage and outright denial. This chapter treats modifications not as isolated specs but as elements that carry legal and financial consequences. It foregrounds the idea that, beyond performance or aesthetics, the legality of changes and the timing of disclosure drive how insurers price risk, what they will cover, and how a claim is adjudicated after an loss occurs.

At the core is a practical rule that many policy documents share: transparency within a defined window—often framed as within ten days of completing a modification—helps preserve coverage. This is more than a bureaucratic courtesy. When a driver informs an insurer about fundamental changes, the company can reassess risk, adjust premiums, and align the contract with the new risk landscape. When disclosure is delayed or avoided, the consequences compound. In some cases, a policy can be voided retroactively, or a claim can be reduced or denied outright because the insurer views the modification as changing the contract’s risk baseline in ways not contemplated by the original terms. This risk is not theoretical; it is a practical obstacle that can render expensive upgrades financially toxic if not managed correctly.

The research into how modifications interact with insurance highlights a spectrum of effects. Performance and power upgrades sit at the top of the risk scale. Engine tuning, turbocharging, or any remapping that increases horsepower and torque alters acceleration, braking dynamics, and even handling characteristics. Insurers interpret these changes as elevated risk—more speed, more torque, more probability of loss from high-energy scenarios. When these alterations are done without informing the insurer, the price of admission to coverage can shift from a simple premium increase to outright refusal of coverage for the modified vehicle. The same logic applies to suspension and chassis work. Lowered ride heights, stiffer springs, or aftermarket dampers can change the way a car behaves under braking, cornering, and on uneven surfaces. The steering feel and stability margins are no longer what the factory designed them to be, and insurers respond accordingly with tighter underwriting criteria or higher premiums.

Cosmetic and aesthetic modifications, while not always directly altering safety mechanics, still warrant disclosure. Changes to wheels and tires can affect steering response, braking distance, and even the accuracy of the speedometer. Speed calculations that inform risk models depend on tire circumference and rolling resistance; when wheels deviate from stock specifications, an insurer’s data inputs shift, nudging premiums upward or triggering a need for a specialized valuation. Body kits and paint jobs influence aerodynamics and structural integrity only when they involve modifications to the car’s frame or essential body components. A visual makeover that does not touch the structural framework might be deemed moderate risk, or merely require a rider on the policy that captures the vehicle’s updated appearance and any safety-related consequences.

Interior modifications occupy a more nuanced space. Upgrades to seats, airbags, and interior fixtures can interfere with safety systems if not installed with risk awareness. Racing seats, different seat rails, or altered mounting points can, in some designs, affect how airbags deploy in an accident. This is a front-line concern because insurers often tie coverage to the integrity of occupant protection systems. A complex installation that creates a potential fire hazard—say, through aftermarket wiring or substandard insulation—can become a claim risk separate from the vehicle’s physical crash dynamics. In such cases, a fire-related claim could be contested if the installation is found to be a contributing factor, even if the fire originates elsewhere in the vehicle. This is where a cautious, methodical approach to modifications converges with insurance policy language.

The distinction between legal and illegal modifications is not merely a private matter between a driver and their garage. It bears directly on policy cancellation and claim denial. In jurisdictions with stringent automotive and safety regulations, modifications that contravene national rules—such as changing engine displacement without authorization, removing critical structural components, or installing lights and sound systems that fail to meet safety standards—can trigger policy voidance. The insurer’s rationale is clear: if a modification violates the law or policy terms, the risk the policy was meant to cover has altered in a way the contract cannot legally accommodate. If an accident occurs, the insurer must decide whether the modifications were a contributing factor, whether the policy remains valid, and how to apportion liability when law and contract collide with the facts of the loss. The practical outcome, in many cases, is claim denial for damages to modified components or, in more severe instances, the denial of the claim entirely on the basis of policy violations.

Where the legal milieu matters most is in public policy implementation and the evolution of insurance regulation. In some places, legal cultures characterized by adversarialism—where dispute resolution is framed as contestation rather than cooperation—create a slower path to updating insurance rules in response to new automotive technologies and common modification practices. Such a climate can extend the period during which insurers operate under outdated legal standards. When liability rules, risk assessment criteria, or claims practices lag behind the realities of modified vehicles, carriers may rely on conservative underwriting models that inflate premiums or narrow coverage options to manage perceived uncertainty. The effect on drivers is tangible: higher costs, fewer options, and more difficulty obtaining legitimate, forward-looking coverage for new kinds of modifications.

The Italian context, as explored in recent scholarship on adversarial legal culture, helps illuminate why this matters for insured drivers, policyholders, and insurers alike. Adversarialism shapes attitudes toward law and reform, and it can slow the adoption of updated rules that would otherwise clarify how modified vehicles should be insured. If regulatory updates are delayed, insurers face a gray zone where liability, risk assessment, and claims processing rely on older frameworks. This can produce higher premiums due to perceived regulatory risk, or reduced coverage where carriers fear legal exposure stemming from ambiguous standards. The tension between a culture that prizes judicial autonomy and the need for practical, timely policy updates underscores a core challenge for modern car insurance: how to balance the safety and reliability of road transport with the realities of a rapidly evolving modification landscape.

For readers who want a more practical entry point into how these dynamics play out in everyday decisions, a focused guide on the specific effects of modifications on insurance is available. It offers concrete steps every driver can take to minimize risk and maximize clarity with their insurer. See the practical discussion here: What Modifications Affect Car Insurance.

The broader takeaway is simple, yet powerful: the law governs what is permissible, but insurance governs the cost and likelihood of payment when things go wrong. The two systems intersect most clearly where modifications cross legal thresholds or where disclosure is imperfect. The ten-day disclosure window is a hedge against future disputes; it preserves the integrity of the contract and helps ensure that the policy liability matches the vehicle’s actual risk profile. When drivers respect this rule, they guard against two kinds of loss—financial waste from unnecessary premium hikes, and the much more consequential risk of claim denial when a modification becomes the unseen precondition of a loss. The onus is on the driver to document changes, retain receipts, and maintain a transparent dialogue with the insurer, so that both parties operate from the same risk calculations.

Looking ahead, this topic does not live in isolation. It connects to how insurers design products, how regulators set standards, and how drivers adapt to the evolving technical landscape of vehicle customization. It invites a pragmatic mindset: plan modifications with the end-to-end insurance outcome in mind. Seek endorsements or riders that explicitly cover the added equipment, maintain detailed records of parts and installation steps, and pursue inspections or approvals that verify safety and legality. In doing so, drivers can navigate the fine line between legal and illegal modifications while preserving the possibility of fair, predictable insurance coverage. The result is not only financial peace of mind but also a safer, more accountable approach to automotive customization.

External reading for those seeking a deeper legal dimension on how adversarial legal culture shapes reform and its consequences for insurance can be found here: https://brill.com/view/journals/ejcc/34/1/article-p1_1.xml

Disclosure as a Cornerstone: How Honest Car Modifications Shape Insurance

Transparency in car modifications is more than courtesy; it is a fundamental pillar of insurance protection. When a vehicle owner asks, implicitly or explicitly, for coverage that reflects the true state of their car, the insurer can assess risk accurately, price it fairly, and tailor protection that remains valid when it matters most. The converse—keeping changes hidden—turns a contract into a fragile agreement that can crumble when a claim is filed. In the world of motor insurance, disclosure is the practical hinge between ownership of a modified vehicle and the financial safeguards that help you ride with confidence. The central idea is simple: insurers base their decisions on a vehicle’s original specifications, the value of the car, and the likelihood of loss. Any modification that shifts those factors—whether by enhancing performance, lifting the value, or altering the risk of damage—requires explicit consideration. When changes are not disclosed, the risk profile shifts in ways the policyholder rarely anticipates, and the consequences can reach far beyond a higher premium. The consequences can reach into claim outcomes, policy validity, and the long-term viability of coverage after an incident. The broad lesson is not to fear modifications, but to approach them with deliberate, documented transparency that aligns the expectations of the driver and the insurer. This alignment is more than a compliance exercise; it is a practical strategy to preserve coverage and even improve safety outcomes through properly understood risk management. \n\nThe landscape of modifications spans a spectrum from performance upgrades that genuinely alter the car’s capabilities to cosmetic tweaks that affect aesthetics as much as risk. Performance and power modifications sit at the heart of risk assessment because they directly influence how a vehicle behaves on the road. Engine tuning, turbocharging, supercharging, or remapping can increase horsepower and torque, elevating acceleration, cornering dynamics, and braking demands. Insurers tend to treat these changes as high-risk adjustments, and when they are suspected or discovered but not disclosed, they can trigger premium surges, coverage refusals, or even policy cancellations. The same logic applies to suspension and chassis alterations. Lowering ride height, installing non-standard springs, or modifying dampers can alter handling, stability, and braking response, especially in emergency maneuvers or on uneven surfaces. In the eyes of underwriters, such changes modify the car’s safety envelope and the perceived likelihood of a claim, which translates into risk-based pricing or, in extreme cases, non-coverage if the modification crosses regulatory or policy boundaries. \n\nCosmetic and aesthetic modifications present a distinct but real set of considerations. Larger or non-standard wheels and tires can affect steering, steering feel, and braking performance, as well as the speedometer’s accuracy. While these may not directly change the mechanical safety of the vehicle, they change the risk equation enough that insurers want to know about them. Body kits, spoilers, or widebody alterations raise questions about aerodynamics and structural integrity, particularly if any kit involves cutting or reinforcing the chassis. Insurance policy terms can be clear that non-factory structural modifications or changes that alter crash behavior may lead to reduced claims acceptance if not properly disclosed. In the interior, changes such as racing seats or specialized harnesses can conflict with airbag deployment logic or restraint systems, creating a potential basis for dispute if an accident occurs and occupant injury is involved. Audio and electrical systems also enter risk scrutiny. High-end installations with complex wiring raise fire concerns if the workmanship is substandard, and a fire traced to aftermarket wiring or improper installation can become a basis for claim denial or policy complications. The overarching thread with these changes is not merely the modification itself, but how well it has been communicated and documented. \n\nA critical distinction in the modification conversation is the legal versus illegal dimension. Modifications that contravene national regulations or nullify a vehicle’s compliance status raise the stakes dramatically. They can void a policy, trigger denial of claims for damages to modified parts, and violate terms that insurers and regulators rely on to maintain the integrity of coverage. The practical implication is clear: any modification that navigates around legally mandated limits, or that removes essential safety features, should be evaluated with expert guidance before proceeding. This is not a barrier to customization, but a reminder that legality and insurer expectations must be part of any decision process from the outset. \n\nAcross this spectrum, the red thread remains constant: inform, document, and align. A common but often overlooked point is the timing of disclosure. Failing to notify your insurer in writing within a defined window after a change is a critical misstep. In many markets, including the guidance circulated by major industry bodies, timely notification preserves the ability to claim for losses involving modified parts and maintains the integrity of the insurance contract. The absence of disclosure can prevent a claim from being paid, even if the accident is unrelated to the modification. On the other hand, proactive disclosure enables the insurer to assess and price the revised risk accurately, ensuring that you retain coverage for the full spectrum of potential losses. It also opens the door to endorsements or specialized coverage that reflect the true state of the vehicle. When a change is substantial, such as a new engine or a significant body kit, many policyholders find value in seeking an Additional Equipment Loss Insurance endorsement or similar coverage that explicitly accounts for the added components. This approach does not simply transfer risk; it calibrates protection so that the financial impact of a loss does not outstrip the value of the modifications themselves. \n\nThe practical path to effective disclosure is straightforward but demands diligence. Before starting any modification, inform your insurer and document the scope of the planned work. While not every modification requires a separate policy amendment, those that alter core risk factors—engine displacement, power output, suspension geometry, or critical safety systems—almost always do. A transparent dialogue helps the insurer understand not only what is being changed, but why and how it affects vehicle performance and occupant safety. It is equally important to retain records of the exact components installed, installation methods, and any professional certification or warranty documentation. These documents serve as a concrete basis for the insurer’s risk assessment and become valuable evidence if a dispute arises later. \n\nFrom a consumer perspective, the discussion often extends beyond mere compliance. Some insurers recognize the potential safety benefits of certain modifications, especially when they are designed to improve braking performance, traction control, or crashworthiness. When modifications contribute to reducing risk or improving the vehicle’s ability to avoid an accident, they can, in some cases, be reflected in premium considerations or discounts. Yet this is not a universal rule, and any perceived savings hinge on transparent communication and the insurer’s willingness to recognize the improvement. The optimal strategy remains to start with open, written disclosure and to pursue endorsements or specialized coverage that explicitly accounts for the changes. It is a collaboration with the insurer, built on trust and written agreement, rather than a unilateral assumption that “modifications are fine.” \n\nThe broader ethical and practical dimension of disclosure ties back to the contract’s integrity. A policy is, in essence, a bilateral agreement, with the insured and the insurer sharing a risk mutuality. When modifications are concealed, the insurer’s fundamental risk model is skewed, which can undermine the contract’s purpose: to protect both sides against genuine financial exposure. By documenting every material change and seeking appropriate endorsements, drivers protect themselves from the risk of post-incident disputes, ensure that their claims align with policy terms, and reduce the chance that a mischaracterized risk will deprive them of coverage at the moment of need. This approach also sustains the long-term value of the insurance relationship. If a driver later decides to sell the car, clear records of modifications and the corresponding coverage can support resale value and reassure prospective buyers that the vehicle’s altered risk profile has been properly accounted for. \n\nFor readers seeking practical guidance beyond general principles, many insurers and trade bodies advocate for proactive disclosure as a standard practice. If you want a concise overview of how modifications can affect insurance and the best practices for disclosure, you can consult a widely referenced resource on the topic. In the spirit of reader-facing guidance, a directly relevant article on the topic is available here: insurance for modified cars. This piece emphasizes the need to forecast how each change shifts risk, the importance of keeping records, and the value in securing endorsements that acknowledge the new configuration of the vehicle. The guidance aligns with a mounting consensus in the insurance community: honesty about modifications is not merely a regulatory obligation but a practical risk-management strategy that protects you, your assets, and your peace of mind on the road. \n\nUltimately, disclosure is about clarity and protection. It is the mechanism by which drivers can customize their vehicles without forfeiting the safety net that insurance provides. When approached thoughtfully, modifications can enhance both performance and safety, particularly when implemented with professional guidance and transparent communication. The insurance contract remains intact, claims are handled according to the true risk, and policyholders retain access to coverage tailored to their modified cars. The message is straightforward: talk early, document thoroughly, and pursue coverage that explicitly reflects the vehicle as it exists today, not as it existed at factory release. For official guidance on how modifications intersect with insurance, reference the sector’s standards as articulated by the UK Association of British Insurers (ABI): https://www.abi.org.uk.

Final thoughts

Understanding the intricate relationship between car modifications and insurance is essential for any vehicle enthusiast. Whether enhancing performance, changing aesthetics, or upgrading interiors, each modification carries its own set of risks and potential consequences regarding insurance coverage. By being aware of the impacts of different types of modifications, the legal constraints involved, and the critical nature of disclosure to your insurance provider, you can safeguard your investment and enjoy your modifications without unnecessary financial resurgence. Remember, a well-informed modifier is a protected modifier.